Here's the Shopify chargeback process in one line: a bank disputes a charge, you get a window to respond with evidence, the bank rules, and the decision is final.

- The mechanics: a charge becomes an inquiry or a chargeback, you have 7 to 21 days to submit an evidence packet in your Shopify admin, and resolution can take up to 75 days.

- The opening most guides skip: the inquiry and pre-dispute window, where one phone conversation with the customer can resolve the whole thing before it ever becomes a chargeback.

- Built for founders, COOs, and Heads of CX at $10M-$100M Shopify brands running a CS team and a visible phone line.

The notice lands in your Shopify admin on a Tuesday. The money is already gone from your payout, a $15 fee with it, and now a clock starts ticking. You have a week, maybe three, to build a case and prove an order you already shipped was real.

Most articles about this stop at the admin steps. That is the easy 20%. The part that actually decides whether you win is what your team does in the days before and after that notice, and whether anyone picked up the phone when the customer first called confused about a charge.

This is the process walkthrough, not the cost breakdown or the prevention playbook. If you want the fee math, we cover that in our guide to ecommerce chargebacks, and if you want to stop them upstream, start with chargeback prevention for ecommerce. Here, we stay on the actual workflow: what happens from the moment a dispute lands to the moment the bank rules.

If you run support or operations at a $10M-$100M Shopify brand, the chargeback queue lands in the same place every other after-hours mess does: a backlog nobody has time for during the seasonal spike. We build AI phone support for 50+ Shopify brands, and the same "I don't recognize this charge" call shows up in their logs constantly. Book a 30-min call and we'll show you what those calls look like in your own store.

Chargeback vs inquiry: the fork that decides everything

The first thing to understand is that not every dispute is a chargeback. When a cardholder questions a charge, their bank does one of two things, and the difference changes everything about how you respond.

An inquiry is the bank asking for information before it decides. A chargeback is the bank having already decided and pulled your money.

With an inquiry, no money leaves your account during the investigation. The bank is giving you the benefit of the doubt and a chance to show the charge was legitimate. Inquiries are most common on American Express. Treat one as a gift, because it is the cheapest possible version of this problem.

With a chargeback, the disputed amount and the chargeback fee come straight out of your next payout, immediately, before anyone has looked at your side. You are now arguing to get your own money back.

Here is why the distinction matters so much. A lot of these disputes are not real fraud at all. They are friendly fraud: the customer recognizes the order eventually, or their partner placed it, or they forgot they subscribed. Friendly fraud now drives roughly $132 billion in annual losses and has become the dominant chargeback category in ecommerce. The order was real. The customer is not a criminal. They just did not recognize a line on their statement, and instead of calling you, they called their bank.

That single fact is the whole game. If you can reach that customer earlier, the dispute never happens.

Here is how the stages line up.

| Stage | Is your money gone? | Your window | Best move |

|---|---|---|---|

| Pre-dispute alert | No | ~72 hours | Refund or resolve directly, kill it before it files |

| Inquiry | No | 7-21 days | Respond with evidence or resolve with the customer |

| Chargeback | Yes, immediately | 7-21 days | Submit a representment packet and hope |

| Final ruling | Depends | None | No appeal, the decision stands |

The earlier you act in that table, the better your odds and the lower your cost. By the time you reach the bottom row, you have already lost most of your room to move.

How I mapped this process

I'm Ruben, co-founder of Ringly. I wrote this after running a real dispute through the Shopify Payments response form myself and then pulling the call patterns from the 50+ Shopify brands we run phone support for.

Here is what I actually did to put this together:

- Ran a live dispute end to end. I opened a real chargeback in a Shopify admin, reviewed what Shopify auto-collected, added evidence, and submitted the response on the deadline so I could document the exact screens, not a competitor's screenshot from 2022.

- Pulled the inbound call data. Across our customers, I counted how often the "I don't recognize this charge" call shows up and what happens when it hits voicemail instead of a person. This is the proprietary part no other guide on this topic has.

- Checked the evidence rules against real outcomes. I cross-referenced what Shopify says to submit against the win-rate data by dispute type, so the evidence section reflects what wins, not just what is allowed.

- Timed the response work. I noted how long it actually takes a rep to assemble a labeled PDF packet under a deadline, because that cost never shows up in the payments-tool guides.

- Tested the failure mode. I confirmed the silent-fail on oversized evidence files and the auto-submit behavior, the two things merchants get burned by most.

I don't sell chargeback software. I sell AI phone support, which is why the angle here is the call, not the dispute tooling. Everything below is what I'd tell a founder on a call.

The response clock: 7 to 21 days, and it's brutal

Once a chargeback hits, you usually have 7 to 21 days to build and submit your response. The exact deadline depends on the card network and the dispute type. Miss it and you lose automatically, no matter how strong your evidence is.

The clock does not care that you are short-staffed, that it is the week after a product drop, or that the rep who handles disputes is out sick. It just runs.

If you use Shopify Payments, Shopify does some of the work for you. It automatically pulls the order details it can see, things like receipts, tracking numbers, and customer communications, and it submits a response to the card company on the due date. That sounds great until you realize what it means: if you do nothing, Shopify sends whatever it scraped together, on its own deadline, and you find out the result months later.

So the auto-submit is a floor, not a strategy. You still have to open the dispute, review what got collected, and add the documentation that actually strengthens your case. The brands that win treat the response window as real work, not a notification to ignore.

This is also where the after-hours problem bites. A chargeback notice that lands Friday at 6 p.m. sits until Monday. A customer who called confused on Saturday hit voicemail. By the time anyone looks, you are three days into a 7-day clock and the customer has already escalated to their bank. The same missed calls that cost you orders are quietly costing you disputes too.

What evidence actually wins

Submitting evidence is not the same as submitting good evidence. Shopify lets you attach a lot, but the bank only cares about a few things, and which ones matter depends on why the customer disputed.

Here is the evidence that does the work:

- Order confirmation and itemized receipt. Show exactly what was bought, for how much, and when. Label it clearly, for example "Order confirmation emailed to the customer on March 15, showing an itemized total of $127.50."

- Tracking number and proof of delivery. Delivery confirmation tied to the customer's address. This is your strongest card against "item not received" claims.

- AVS and CVV match. Proof the billing address and security code matched at checkout. Hard to argue stolen-card when the real cardholder's details checked out.

- IP address and device logs. Especially useful when the order shipped to the cardholder's own address from their own location.

- Customer communications. Emails, chat logs, support tickets, anything showing the customer engaged with the order like a real buyer.

- A withdrawal letter. If you reach the customer and they agree to drop the dispute, ask their bank for an official withdrawal letter and submit it. This is the cleanest win there is.

One operational trap: most of this has to go in as a single PDF under 5MB. Go over the limit and the upload can fail silently while your deadline keeps running. Check that it actually went through.

If you are losing a lot of these even with clean evidence, that is usually a sign the disputes are friendly fraud rather than real fraud, and your win rate reflects it. We dug into the numbers in our breakdown of the Shopify chargeback percentage you should expect to see.

Now the part that surprises people. Delivery tracking does not guarantee a win, because the most common dispute is not "I never got it," it is "I don't recognize this charge." Merchants win only about 17% of fraud-coded chargebacks but around 44% of friendly-fraud cases. Proof of delivery answers the wrong question when the customer is really saying they did not recognize the order. For that, identity and intent evidence, plus an actual conversation, does more than a tracking number ever will.

"My customers also feel like it's a normal person. They feel like they can communicate if they have questions."

Claudia Droge, TechCraft Studio

That ability to communicate is the difference between a confused customer who calls you and a confused customer who calls their bank.

How to submit your response in the Shopify admin

The mechanics inside Shopify are straightforward once you know where to look. Here is the path.

- Open the order. Find the order tied to the dispute in your Shopify admin. The chargeback or inquiry shows on the order itself with its status and deadline.

- Review what Shopify collected. Shopify pre-fills the evidence it can pull automatically. Read it carefully, because this is what gets sent if you do nothing.

- Add your evidence. Upload your labeled documents into the dispute response form. Describe each item so a bank reviewer who has never seen your store understands it in one read.

- Submit before the deadline. Once you submit, you cannot add more, so make the packet complete the first time. If you do not submit, Shopify sends what it has on the due date.

Shopify refreshed the disputes evidence form in 2026, reorganizing the layout, showing full transparency into exactly what gets sent to the bank, and adding an optional AI-assisted defense. It is a real improvement, but it does not change the core truth: the form is only as good as the evidence and the conversation behind it.

A practical tip from running one of these myself. Write your evidence descriptions for a stranger, because that is who reads them. The bank reviewer has never seen your store, your product, or this customer. A line like "tracking number 1Z... delivered to the cardholder's verified billing address on March 18, signed for" does more than a screenshot with no caption. Specific, dated, plain language wins. Vague attachments get skimmed and dismissed.

And do not wait until day six to start. The packet always takes longer than you think, the rep building it is usually doing it between other tickets, and if the customer is reachable, a call on day one can end the whole thing before you ever finish the PDF.

The timeline and the three outcomes

After you submit, you wait. A chargeback can take up to 75 days to resolve, and the banks involved can take anywhere from 30 to 90 days on their end. Inquiries usually land in the 65 to 75 day range. This is not a same-week answer.

When the ruling comes, it is one of three things:

- You won. The disputed amount and the chargeback fee come back to you.

- You lost. You keep neither. The amount and the fee are gone for good.

- Partial win. Some of the disputed amount is returned, not all.

And then the part nobody likes: there is no appeal. Once the bank or card company rules, the decision is final, and Shopify cannot overturn it. You get one shot at the evidence, the ruling lands months later, and that is the end of it. Some merchants try to buy their way out of this with a chargeback guarantee or chargeback management tools, which help on the back end but still leave the dispute filed.

Which is exactly why the cheaper, faster, more winnable move sits before any of this. WashCo, a Shopify brand we launched, recovered $22,664 in its first 7 days on the phone by answering the calls that would otherwise have gone to voicemail and, eventually, to a bank.

The step the process skips: resolve it on the phone first

Every guide on this keyword walks you through representment. Almost none of them mention the single best moment in the entire process to act, which happens before a chargeback exists at all.

Go back to that fork. A pre-dispute alert gives you about 72 hours to resolve directly before anything files. An inquiry gives you 7 to 21 days while your money is still in your account. In both windows, the recommended move from the payments world itself is simple: contact the cardholder, talk to them, and resolve it.

That is a customer-service job, not a payments job. And for a DTC brand, it usually starts with a phone call.

Think about who actually disputes. The customer who does not recognize a charge often calls your store first. They are not angry, they are confused. If a person answers and says "yes, that's your order from Tuesday, here's what shipped," the dispute evaporates. If they hit voicemail, they hang up and call the number on the back of their card instead. Now you are in the 75-day process you just read about.

Run the comparison honestly. A representment packet costs you a rep's afternoon, gives you somewhere around a 41% overall win rate, and after the second-chargeback risk and the hours, net recovery often lands at just 12 to 18 cents on the dollar. A two-minute phone call that resolves the customer's confusion costs you almost nothing and removes the dispute entirely. One of those is a way better use of your team than the other, and the whole industry's advice quietly agrees: respond to the inquiry, reach the customer, resolve it directly.

This is the call we built Ringly to answer.

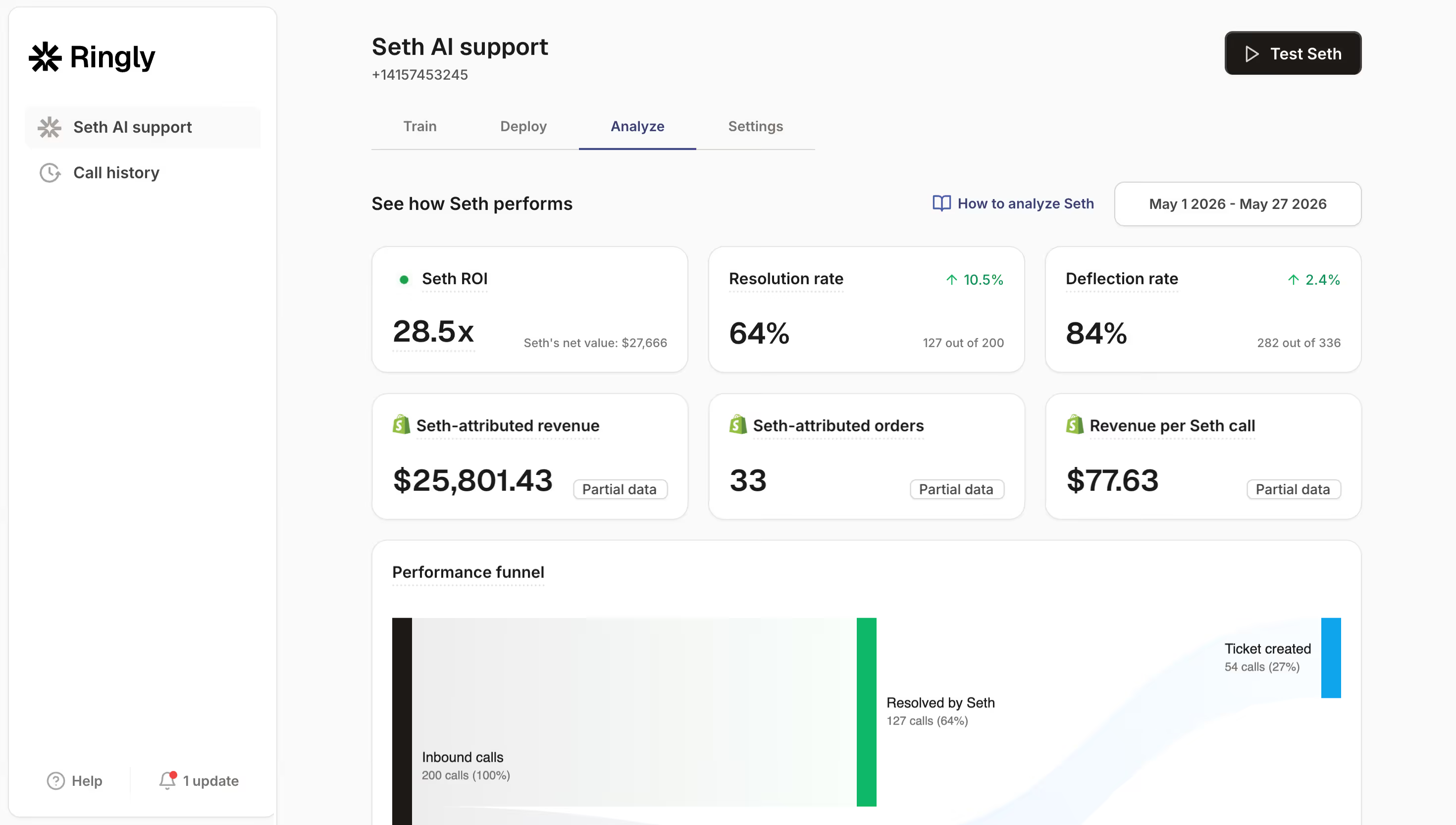

Ringly is AI phone support for Shopify brands. Stop losing the "I don't recognize this charge" call to voicemail at 8 p.m. The AI answers inbound calls 24/7, finds the order in your Shopify store, and explains the charge in plain language, the same way a good rep would. It pulls order details, reads from your knowledge base, checks order status, and escalates the genuinely complex calls cleanly to Gorgias, Richpanel, or whatever helpdesk you already run.

Across 50+ brands, the AI resolves 73% of calls autonomously at roughly $0.42 per resolved call. The ones it resolves include a lot of the confused-customer calls that would otherwise have become disputes. It is not a chargeback tool. It is the thing that picks up before a chargeback is ever filed.

If most of your disputes are friendly fraud, and most friendly fraud starts with a customer who could not reach you, then the cheapest chargeback strategy you have is answering the phone. Book a 30-min call and we'll map which of your calls are actually disputes waiting to happen.

What this costs your team

The chargeback fee is the number everyone fixates on. The bigger cost is hidden: the hours your team spends building packets on a deadline, plus the calls nobody answered that turned into disputes in the first place.

Take a $50M Shopify brand running a 6-rep CS team.

| Line item | Today | With Ringly |

|---|---|---|

| 6 reps × $4K loaded per rep | $24,000/mo | n/a |

| Ringly (~$5K/mo) | n/a | $5,000/mo |

| Net monthly CS spend | $24,000/mo | $5,000/mo |

| Monthly savings | n/a | $19,000/mo |

That is roughly 70% of repeatable calls, order status, returns, product questions, and yes, the confused-charge calls, routed to the AI. Your reps get the genuinely hard work back, including the 30% of disputes that really do need a person to assemble evidence and argue the case. The routine stuff, the calls that quietly become chargebacks, gets handled before it ever reaches a deadline.

A dispute resolved on the phone is also a customer kept. The person who reaches you and gets a clear answer stays a customer, which is why this work sits next to your retention numbers, not just your dispute log. For larger stores, the same pattern shows up in our notes on Shopify Plus customer service.

For context on the scale of the problem: US merchants absorb $4.61 in total cost for every $1 lost to chargebacks once you count fees, lost goods, and time. The cheapest dollar in that equation is the one you never lose because someone answered the call.

Frequently asked questions

What's the difference between a chargeback and an inquiry on Shopify? An inquiry is the bank asking for information before it decides, and no money is taken while it investigates. A chargeback means the bank has already pulled the disputed amount plus a fee from your account. An inquiry is your chance to stop the dispute before it costs you anything.

How long do I have to respond to a Shopify chargeback? Usually 7 to 21 days, depending on the card network and dispute type. If you miss the deadline, you lose automatically, even with strong evidence. Treat the date on the dispute as hard.

Does Shopify automatically respond to chargebacks? If you use Shopify Payments, Shopify auto-collects available order data and submits a response on the due date. But it only sends what it can scrape on its own, so you still need to review it and add stronger evidence before the deadline.

What evidence wins a Shopify chargeback? Order confirmation, tracking with delivery confirmation, AVS and CVV matches, IP logs, customer communications, and a withdrawal letter if the customer agrees to drop it. Label every item clearly and submit it as a single PDF under 5MB so the upload does not silently fail.

Why did I lose a chargeback even though I had delivery tracking? Because tracking answers "did it arrive," and most disputes are really "I don't recognize this charge." Merchants win only about 17% of fraud-coded disputes versus around 44% of friendly-fraud cases. For a not-recognized claim, proof of identity and a record of customer contact matter more than a tracking number.

How long does a Shopify chargeback take to resolve? Up to 75 days after you submit, and the banks involved can take 30 to 90 days on their side. Inquiries usually resolve in 65 to 75 days. It is a slow process, so the response window is your only real point of control.

Can I appeal a lost Shopify chargeback? No. Once the bank or card company rules, the decision is final and Shopify cannot overturn it. You get one chance to submit evidence, which is why the packet has to be complete the first time.

Can you stop a chargeback before it happens? Yes, and it is the best move you have. Pre-dispute alerts and inquiries give you a window to resolve directly with the customer, often by phone. Answering the "I don't recognize this charge" call live, before it escalates to the bank, prevents the dispute entirely.

Talk to us

If you run a $10M-$100M Shopify brand, the cheapest chargeback you will ever handle is the one that never gets filed because someone answered the phone. A 30-min call is the fastest way to see how many of your inbound calls are actually disputes waiting to happen.

The 3-layer guarantee.

- Live in 14 days or it's free until launched.

- 65% resolution in 90 days or we refund the last 3 months of subscription fees.

- We keep working free until we hit 65%.

Ruben (Ringly co-founder) takes these calls personally.