This guide in 30 seconds.

- You'll learn the four sets of rules that govern a Shopify chargeback: Shopify Payments policy, card-network reason codes, the dispute clock, and your own written store policy.

- Around 61% of disputes are now friendly fraud, and an answered phone sits upstream of most of them.

- Built for $10M-$100M Shopify brands watching chargebacks come out of their payouts every month.

A chargeback is not a refund. When one lands, the bank pulls the money plus a fee straight out of your next payout, and Shopify is not on the hook for it. You are.

Most operators learn this the expensive way. If you run a $10M-$100M Shopify or Shopify Plus brand, the chargebacks you lose are rarely the ones you couldn't win. They're the ones nobody answered in time, with a policy that said nothing, on a dispute that started as a phone call you missed.

Here's the part that gets skipped: there isn't one chargeback policy. There are four sets of rules stacked on top of each other, and you need all four. Shopify Payments has its rules. The card networks have theirs. The dispute clock is its own rule. And your own published store policy is a rule too, because the card networks treat it as evidence.

Most $30M+ Shopify brands eat a handful of chargebacks out of their payouts every month and never connect them back to the support line that rang out. We've launched AI phone support for 50+ Shopify brands fighting exactly that leak. Book a 30-min call and we'll walk through where your disputes are actually coming from.

What Shopify's chargeback policy actually says

Start with the part Shopify controls, because it's the part most merchants get wrong.

Shopify is not liable for your chargebacks. Its own policy states plainly that Shopify isn't liable for chargebacks that happen on the platform. When you use Shopify Payments, the disputed amount comes out of your next available payout the moment the chargeback is filed. You don't get a grace period to dispute it first. The money is gone, and you fight to get it back.

On top of the disputed amount, there's a fee. For US merchants, Shopify's chargeback fee is $15 per chargeback, per Shopify's help documentation. If you win the dispute, you get the disputed amount back, and Shopify may refund the fee depending on your country or region.

There's an important distinction Shopify draws between an inquiry and a chargeback. With a chargeback, the bank takes the disputed amount plus the fee right away. With an inquiry, it doesn't. An inquiry is a request for information before things escalate, which means it's your best shot at resolving the issue before money moves. Treat inquiries as the cheap early warning they are.

One more rule on Shopify's side: your chargeback rate matters to your account. A high rate can affect your Shopify Payments status and your eligibility for features. Cross the threshold and you can land in a monitoring program, which opens the door to fines or restrictions on your ability to process payments at all. A chargeback policy isn't just about winning disputes. It's about staying inside the rate that keeps your payments turned on.

Shopify does offer one safety net. Shopify Protect covers fraud-based chargebacks for eligible orders: Shopify eats the order cost and the chargeback fee and manages the dispute for you. The catch is the scope. Shopify Protect is US-only, it needs a US Shopify Payments account, and it covers fraud chargebacks specifically. It does nothing for "I never got it," "it's not as described," or "I cancelled and got charged anyway." Those are on you.

The card networks set the real rules: reason codes

Shopify sits in the middle of every dispute, but it doesn't decide them. Shopify is the payment facilitator. It bundles your evidence and passes it upstream to the acquiring bank and the card network, and the issuing bank plus the network make the ruling. The rules they rule by are reason codes.

There are roughly 151 reason codes across the four major networks (Visa, Mastercard, American Express, Discover), per chargeback-industry references from chargebacks911. Each one carries its own evidence requirements and its own win odds. A fraud dispute with no device data attached is nearly unwinnable. A "not received" dispute with a carrier scan showing delivered is almost always recoverable. Same store, opposite outcomes, decided by which code got filed.

Visa organizes its codes into four buckets: fraud, authorization, processing errors, and customer disputes. A few you'll see often:

- 10.4 (fraud, card-not-present): the cardholder says they didn't make the purchase. The hardest to win without strong order data.

- 13.1 (merchandise not received): the customer says it never arrived. This one lives or dies on tracking and delivery proof.

- 13.2 (cancelled recurring): they were charged on a subscription they say they cancelled.

- 13.3 (not as described or defective): they got it, but claim it wasn't what was promised.

- 12.x (processing errors): duplicate processing, wrong amount, that family of issues.

Mastercard uses its own four categories: authorization, cardholder disputes, fraud, and processing errors. Different code numbers, same logic. The reason code, not your side of the story, decides what evidence you need and whether you have a case at all.

Shopify translates all of this into eight plain-language reasons inside your admin, and tells you exactly what evidence helps each one. This is the part worth memorizing, because it doubles as a checklist for what to capture on every order.

| Shopify reason | What the customer is claiming | Evidence Shopify says helps |

|---|---|---|

| Fraudulent | They didn't authorize the charge | Fulfillment date, billing info, IP and country, tracking |

| Unrecognized | They don't recognize your name on the statement | Fulfillment date, billing info, IP and country, tracking |

| Duplicate | They were charged twice for one item | Why two charges exist, receipts, customer messages |

| Subscription canceled | Charged after cancelling | Cancellation policy, cancellation emails, where the policy was shown |

| Product not received | It never arrived | Fulfillment date, billing info, tracking, activity logs |

| Product unacceptable | Defective, damaged, or not as described | Tracking, product descriptions and photos, return or replacement offers |

| Credit not processed | Reported a return but wasn't refunded | Refund and return policy, where it was communicated, refund emails |

| General | Doesn't fit the others | Order details, comms, shipping confirmations, prior refunds, withdrawal letters |

Notice the pattern. For four of the eight reasons, the winning evidence includes your own policy or your own customer communications. That's not a coincidence, and it's the layer most stores never set up.

Dispute timelines: the deadline is what loses you the money

Reason codes decide whether you have a case. The clock decides whether you get to make it.

Cardholders get a long runway. On both Visa and Mastercard, a customer generally has up to 120 days from the transaction or the expected delivery date to file. That means a chargeback can show up four months after an order you'd long forgotten about.

Your runway is shorter and stricter. Visa gives merchants a uniform 30 days to respond at each phase of a dispute, starting the day after Visa opens that phase. Mastercard gives 45 days regardless of reason code. In practice, the evidence window Shopify surfaces in your admin often reads tighter, around 7 to 21 days, so don't trust your memory of the network rule. Trust the deadline Shopify shows you. Miss it and the case closes against you automatically, with no appeal.

Submitting your evidence is called representment. You assemble the proof, Shopify packages it and sends it upstream, and then everyone waits. Per chargeback-industry timelines, the review and ruling phase can run up to 75 days, and the banks themselves can take 30 to 90 days to update the outcome. So a dispute filed today might not resolve until next quarter, and the disputed cash is sitting outside your payouts the entire time.

One newer rule worth knowing: Compelling Evidence 3.0 went live in April 2026. For "unrecognized" and friendly-fraud disputes, it lets you submit proof that the same cardholder previously bought from you without disputing, which can clear the dispute and even pull it back out of your fraud-rate calculations. It's the closest thing to a retroactive defense the networks offer.

The brutal truth in the data: most lost disputes aren't unwinnable, they're unanswered. A missed deadline loses you a chargeback you'd have won on the evidence. The single most valuable move in your whole policy is a process that never lets the clock run out.

What your own chargeback policy should say

Here's where most Shopify brands leave money on the table. Your published store policy is not just legal housekeeping. The card networks treat it as evidence, and Shopify literally asks for it on two of the eight dispute reasons.

On a "credit not processed" dispute, Shopify wants your refund and return policy and proof of where the customer saw it. On a "subscription canceled" dispute, it wants your cancellation policy and the reminder emails you sent. If those don't exist, or exist but were never shown to the customer at checkout, you've already lost those disputes before they're filed.

So write the policy that becomes your evidence. At minimum, publish and timestamp:

- A clear refund window and conditions. How many days, what state the product has to be in, what's final sale. Make the customer accept it at checkout so there's a record.

- A return process. How they start it, who pays return shipping, how long refunds take to land. This is the language that answers "credit not processed."

- Subscription cancellation steps plus your reminder cadence. Exactly how to cancel, and the emails you send before each renewal. This is what beats "subscription canceled" disputes.

- Shipping and delivery terms. Carriers, timeframes, what happens to lost packages. Tracking is your defense on "not received," and your policy sets the expectation.

- A recognizable billing descriptor. The name on the credit card statement should match your brand, not some processor string. Half of "unrecognized" disputes are customers who really don't recognize the charge.

- A visible contact method and hours. A phone number and email the customer can actually reach before they call their bank instead.

This matters more than it used to because of who's filing. Around 61% of disputes now come from friendly fraud, where the customer did receive the order and disputes anyway, and first-party fraud has climbed to 36% of all reported fraud, up from 15% in 2023, according to chargeback-industry data. Against a friendly-fraud claim, a clear policy the customer demonstrably agreed to is the thing that flips the ruling.

If you want the deeper prevention playbook, we've written it up in our chargeback prevention guide. But policy on paper is only half the job. The other half rings while nobody's at the desk. If your disputes are creeping up, book a 30-min call and we'll talk through your case.

The cheapest chargeback prevention is an answered phone

Look back at Shopify's eight reasons and one thing jumps out. The two that dominate ecommerce, "unrecognized" and "product not received," are the same two phone calls a Shopify brand misses most. "I don't recognize this charge on my statement." "Where is my order?"

A customer with one of those questions has a choice. Call you, or call their bank. When the phone rings out to voicemail at 8pm, plenty of them skip straight to the bank, and now a thirty-second answer has become a 90-day dispute that costs you the order plus $15. The chargeback policy is downstream. An answered phone is upstream, and it's the cheapest prevention you have.

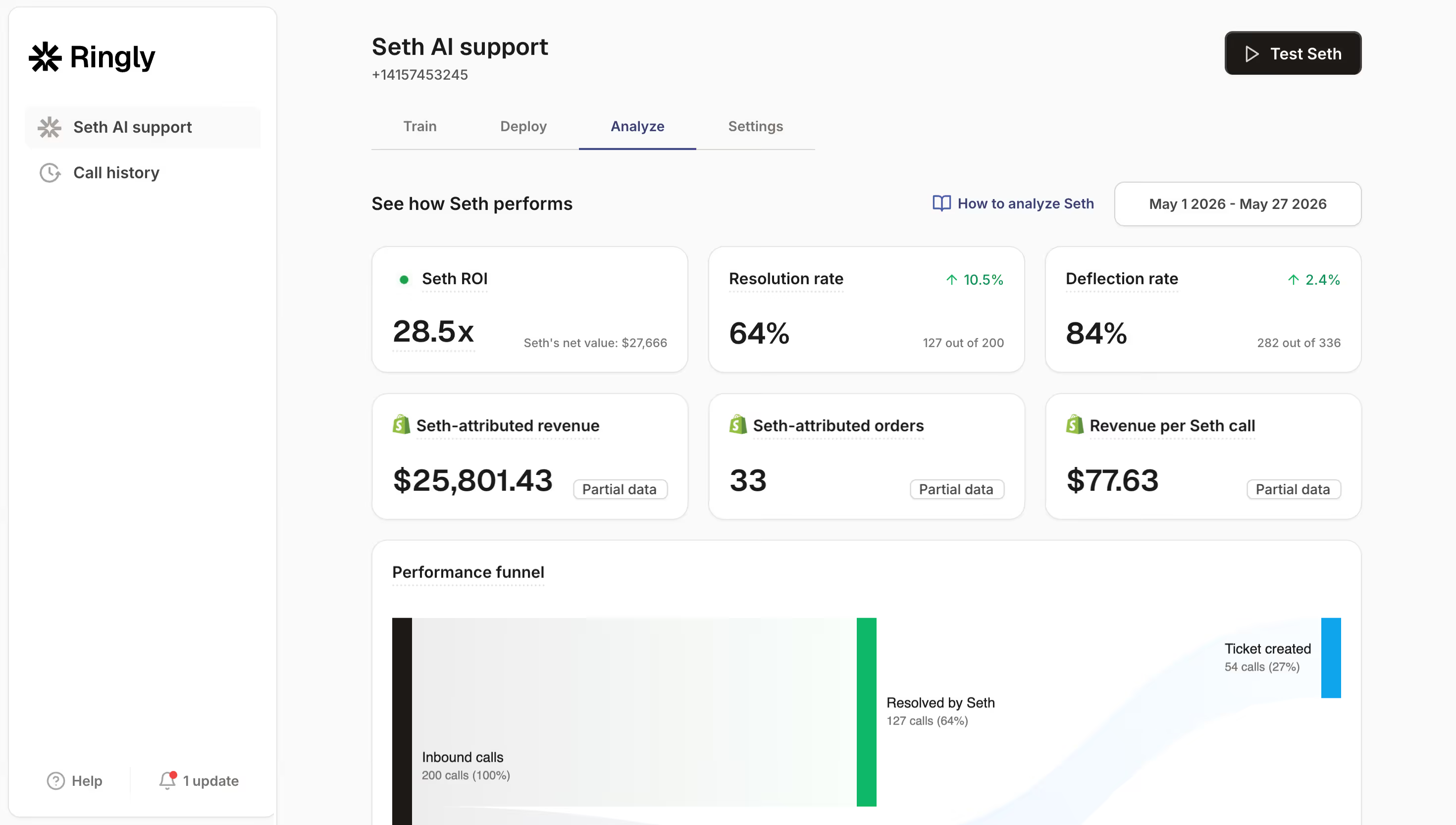

This is the gap Ringly.io closes. It's AI phone support for Shopify brands. Instead of growing a phone team every time call volume climbs, the AI takes the routine inbound calls 24/7: it finds the order in Shopify and reads back the tracking on a where's-my-order call, explains the billing descriptor on an unrecognized charge, and walks a customer through your return policy before they reach for the dispute button. Across 50+ brands, the AI resolves 73% of calls on its own at roughly $0.42 per call, and the hard calls escalate cleanly to whatever helpdesk you already run.

"My customers also feel like it's a normal person. They feel like they can communicate if they have questions."

Claudia Droge, TechCraft Studio

The payoff isn't only fewer disputes. WashCo, a Shopify brand we launched, recovered $22,664 in its first 7 days on the phone, mostly from orders that would otherwise have rolled to voicemail. Answer the call, keep the order, never see the chargeback.

The math holds even before you count the disputes you avoid. Take a $50M brand running a 6-person support team to cover the phones:

| Line item | Today | With Ringly |

|---|---|---|

| 6 reps at $4K loaded each | $24,000/mo | n/a |

| Ringly (illustrative) | n/a | $5,000/mo |

| Net monthly support spend | $24,000/mo | $5,000/mo |

| Monthly savings | n/a | $19,000/mo |

That's roughly 70% of repeatable calls (order status, billing questions, returns) handled by the AI, with the genuinely tricky calls still going to your team. Every one of those answered calls is a dispute that never gets a chance to be filed. If you want to see where your own disputes trace back to, book a 30-min call and we'll do the math live against your call volume.

Frequently asked questions

Who pays for a Shopify chargeback? You do. Shopify states it isn't liable for chargebacks on the platform, and with Shopify Payments the disputed amount comes straight out of your next payout. The one exception is Shopify Protect, which covers eligible fraud chargebacks for US merchants on a US Shopify Payments account.

What is the Shopify chargeback fee? For US merchants, Shopify charges $15 per chargeback on top of the disputed amount, per its help documentation. If you win the dispute you get the disputed amount back, and Shopify may refund the fee depending on your country or region.

What is the difference between an inquiry and a chargeback? With a chargeback, the bank pulls the disputed amount plus the fee from you immediately. With an inquiry, it doesn't take any money yet, it just requests information. An inquiry is your earliest and cheapest chance to resolve the issue before it escalates into a full chargeback.

Does Shopify Protect cover all chargebacks? No. Shopify Protect covers fraud-based chargebacks only, and only for US merchants with a US Shopify Payments account. It does nothing for "not received," "not as described," or "subscription cancelled" disputes, which you have to fight yourself.

How long do I have to respond to a Shopify dispute? The network rules give merchants 30 days per phase on Visa and 45 days on Mastercard, but the practical deadline is whatever Shopify shows in your admin, often 7 to 21 days. Miss that deadline and the case closes against you automatically with no appeal, so the admin date is the only one that matters.

Can my refund policy actually help me win a chargeback? Yes. Shopify asks for your refund and return policy as evidence on "credit not processed" disputes and your cancellation policy on "subscription cancelled" disputes. A clear policy the customer accepted at checkout is often what flips a friendly-fraud ruling in your favor.

Talk to us

If you run a $10M-$100M Shopify brand and your chargebacks are creeping up, the fastest fix usually isn't a better dispute tool. It's answering the calls that turn into disputes in the first place. A 30-min call is the quickest way to see which of your disputes trace back to a phone that rang out.

The 3-layer guarantee.

- Live in 14 days or it's free until launched.

- 65% resolution in 90 days or we refund the last 3 months of subscription fees.

- We keep working free until we hit 65%.

Ruben (Ringly co-founder) takes these calls personally.

Book a 30-min call and we'll talk through your case. Or compare us to your current setup on our Shopify customer service page and refunds guide first.