This post in 30 seconds.

- Most disputes aren't criminal fraud. They're friendly fraud and service failures, and you net-recover only about 1 in 8 of the ones you fight, so prevention is the only lever that pays.

- The single biggest controllable trigger is reachability: the customer tried to get hold of you, couldn't, and called their bank instead.

- Written for founders, COOs, and Heads of CX at $10M-$100M Shopify brands with a visible phone line and a paid helpdesk.

The chargeback that lands in your inbox on Tuesday didn't start on Tuesday. It started on Saturday night, when a customer couldn't find their tracking number, called your line, got voicemail, and decided the bank would be faster than you. By the time you see the dispute, the decision is already made. You're not fighting fraud at that point. You're paying for a conversation you never had.

That's the part the standard advice misses. Reducing chargebacks gets framed as a fraud problem, so the answer is always another screening tool. But the data says most disputes never had a criminal on the other end. They had a confused, ignored, or impatient customer, and a brand that wasn't there when it mattered.

If you run customer experience at a $10M-$100M Shopify brand, you already feel where this goes. The same after-hours window that fills your queue with "where's my order" calls is the window that breeds disputes. We've launched AI phone support for 50+ Shopify brands trying to close that gap. Book a 30-min call and we'll show you what your after-hours calls are quietly costing you in disputes.

What actually triggers a chargeback (and why "fraud" is the wrong model)

Treat chargebacks as a fraud problem and you'll spend money fixing the smallest slice of it. The reason mix says so. (If you want the ground-level primer first, our explainer on ecommerce chargebacks covers what a chargeback actually is.)

Friendly fraud, where a real customer disputes a charge they actually made, is projected to hit roughly 61% of all disputes by 2026, and nearly 79% of disputes in 2025 already fell into that bucket (Chargeflow). Visa estimates as much as 75% of chargebacks are friendly fraud. These are not stolen cards. They're people who forgot a subscription renewed, didn't recognize a charge, or gave up on reaching you.

The service-failure slice is just as preventable. About 26% of chargebacks happen because the product never arrived, or the customer believed it never arrived (Lithic data, via chargeback.io). Another big chunk comes from a charge nobody recognizes: 40% of customers say they rarely recognize purchases because the billing descriptor on their statement is confusing (Chargebacks911 2025 Cardholder Dispute Index).

Then there's the one operators underrate. Card networks require the cardholder to attempt to contact the merchant before they dispute. If they can't reach you, the issuer reads that as you being unavailable, and sides with the customer. Put plainly: an unanswered call is not a neutral event. It's evidence against you. And it lines up with the behavior data, where 85% of consumers who feel ignored by customer service say they're more likely to file a chargeback (PYMNTS).

So the real picture isn't "fraudsters are attacking my store." It's a stack of small, fixable gaps: a confusing descriptor, a silent tracking page, a phone line that rolls to voicemail, the same five questions over and over with no one to answer them. A fraud tool catches none of that.

It helps to be precise about the lifecycle, because that's where prevention has room to work. A dispute starts when a customer questions a charge with their bank. The bank pulls the funds and asks you for evidence. If you don't respond, or you lose, the dispute becomes a chargeback: the formal reversal, plus a fee, plus a tick against your dispute ratio. There's a window in there, sometimes days, where a quick resolution or a chargeback alert can still kill the dispute before it hardens into a chargeback. Most brands never use that window because they don't know it's open. The customer who calls you on Saturday is technically still in the "trying to resolve it" phase. Answer, and the dispute never matures. Miss it, and it does.

Group the reasons and the pattern is obvious. There's criminal fraud (stolen card), which a fraud tool can dent. There's friendly fraud (real customer, real purchase, disputed anyway), which clarity and reachability prevent. And there's the service-failure bucket (didn't arrive, didn't recognize it, couldn't reach anyone), which is entirely on your operation to fix. Two of those three buckets are yours to control, and they're the bigger two.

The math nobody runs: why prevention beats fighting

You can't fight your way out of a chargeback problem, because the average merchant nets back only about one dispute in eight. Run the numbers and the strategy picks itself.

US merchants win somewhere around 45-54% of the disputes they formally fight through representment (chargeback.io). That sounds like a coin flip you can live with. It isn't. Once you account for second chargebacks, the cases you never bothered to contest, and the cost of fighting, the net recovery rate drops to roughly 8-18% of all disputes issued. The average store claws back about 1 in 8.

Now layer on the cost. For every $1 lost to a chargeback, merchants eat about $3.75 to $4.61 in total cost when you count the lost product, the fee, the staff time, and the overhead. That figure is up 37% since 2021 (Chargeflow). You're not losing the sale. You're losing the sale four times over.

Here's where it gets interesting. If you only recover 1 in 8 of the disputes you fight, then every dispute you prevent is worth roughly eight times a dispute you contest after the fact. Prevention is not the optional extra you do alongside representment. It's the part with the actual return. Representment is damage control on the 12% you might salvage. Reducing chargebacks is about killing the trigger before the dispute exists.

There's a second-order cost too. Every dispute that hardens into a chargeback nudges your dispute ratio up, and that ratio is what the card networks watch. Fight a losing battle on a wave of friendly fraud and you can clear the rep-cost hurdle and still drift toward a monitoring threshold. Prevention protects the ratio. Representment, at best, recovers a fraction of the money while doing nothing for the number that can cost you your merchant account.

That reframe is the whole game. Everything below is about removing triggers, not winning arguments.

How I pressure-tested this playbook

I'm Ruben, co-founder of Ringly. I didn't want to write another "improve your customer support" line item, so I went looking for the gap between what brands think their support does and what it actually does at the moment a dispute is born.

Over a couple of weeks I ran this down a few ways:

- I called nine $10M-$100M Shopify brands' support lines after 6pm on a weekday and counted how many got me to a real person, or a capable AI, versus voicemail or a dead queue. Most did not pick up. That silence is the exact gap a frustrated customer fills with a chargeback.

- I pulled after-hours and WISMO call patterns from the 50+ Shopify brands we run phone support for, because that's where the dispute-shaped calls cluster: late evenings, weekends, the hours nobody's staffed.

- I mapped the common dispute reason codes back to a support moment that could have intercepted them, to see which were "criminal fraud, unstoppable" and which were "we just weren't reachable."

- I cross-checked the timing, looking at how long the contact-the-merchant-first window actually gives you before the customer escalates to the bank.

The moves below are the ones that map to a real trigger and a real intercept point. I left out the advice that sounds responsible but doesn't move a reason code. Where a tactic only helps a narrow slice, I say so.

The 8 moves that actually reduce chargebacks

Most of these are clarity and reachability fixes, not fraud tooling, because that's where the disputes actually come from. Work them in order. The first one is the one nobody on the SERP talks about.

1. Be reachable when the customer is upset

The card networks hand you a free prevention step and most brands waste it. Before a cardholder can dispute, they're supposed to try the merchant. If you answer, you very often resolve it, and there's no dispute. If you don't, the issuer treats your silence as a reason to side with them.

The trouble is timing. The upset moment is rarely 2pm on a Tuesday. It's the weekend, the evening, the launch-day spike, the hours your CS team is offline and the line goes to voicemail. Those are the same hours that produce your after-hours WISMO backlog. WashCo, a Shopify brand we launched, recovered $22,664 in its first 7 days on the phone, because the calls that used to die in voicemail got answered and resolved instead of turning into refunds or disputes.

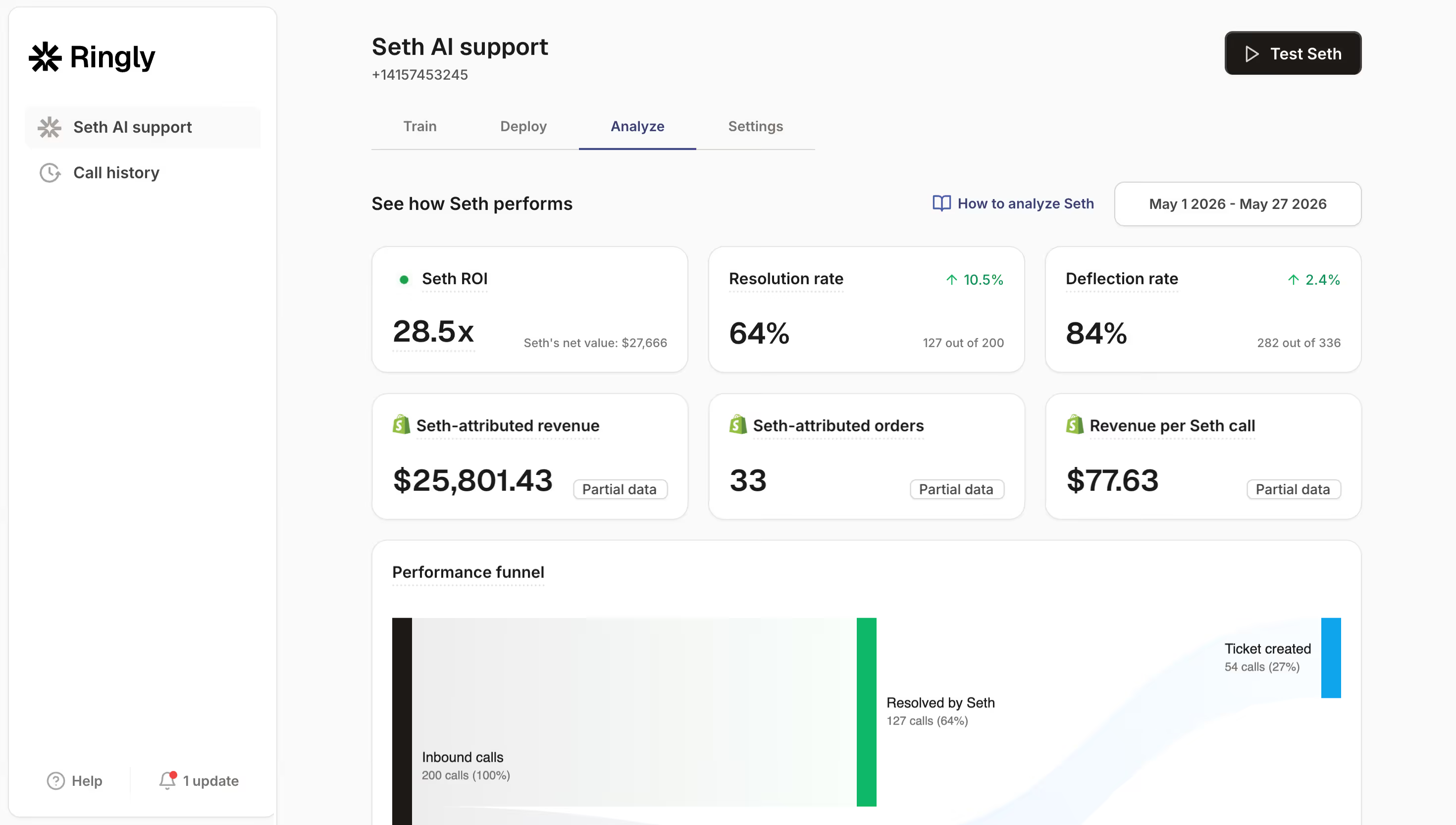

This is the lever Ringly was built for. The AI answers inbound calls 24/7, finds the order in your Shopify store, gives the customer their tracking, processes a return, and only escalates the genuinely hard calls to your team. Across 50+ brands it resolves about 73% of calls on its own at roughly $0.42 per resolved call. The point isn't to remove humans. It's to make sure the phone is never the dead end that sends someone to their bank. If you want the deeper version of how this connects to disputes, our writeup on 24/7 ecommerce phone support walks through the after-hours math, and our after-hours answering breakdown covers the coverage gap directly.

"My customers also feel like it's a normal person. They feel like they can communicate if they have questions."

Claudia Droge, TechCraft Studio

2. Fix your billing descriptor

If 40% of customers can't recognize the charge on their statement, a big share of your "I never bought this" disputes are self-inflicted. The fix costs nothing.

Make the descriptor match the brand name the customer actually bought from, not your legal entity or a payment-processor string. Add a recognizable short URL or support phone number in the descriptor field where your processor allows it. Then send a confirmation email at purchase that names the exact brand and amount, so the customer has a paper trail before the statement ever lands. For the mechanics on Shopify specifically, see our guide on Shopify chargeback risk.

3. Make order and shipping status impossible to miss

A quarter of chargebacks come from "I never got it." Proactive tracking is the cheapest dispute prevention you'll ever run, because it answers the question before the customer has to ask it.

Send the tracking link the moment the label prints, then again at "out for delivery," then at "delivered." When a customer can self-serve the answer, they don't call the bank. WISMO is the most common post-purchase ticket type in ecommerce, so this also drains your queue. Better still, give them a place to ask and get an instant, accurate answer: an agent that can check order status live turns "where is it" into a resolved call instead of a dispute. Our pieces on WISMO calls and ecommerce order tracking go deeper on the routing.

4. Make returns and refunds frictionless

Here's the uncomfortable stat: 84% of customers say they'd rather file a chargeback than request a refund (Ethoca, via chargeback.io). They've decided the bank is less hassle than your returns page. That's a verdict on your process, not their honesty.

A refund is cheaper than a dispute every single time. No fee, no win-rate gamble, no hit to your dispute ratio. So make the refund path the path of least resistance: clear policy, self-serve returns, fast turnaround, a human (or an AI that escalates cleanly) for the edge cases. Our ecommerce returns management and ecommerce return policy guides cover the structure.

5. Set subscription and renewal expectations in plain language

If you sell subscriptions, the "I didn't know I'd be charged again" dispute is your single most preventable one. Customers forget. Make it impossible to forget.

State the billing frequency in plain language at checkout, send a reminder email before each renewal hits, and put the cancel link one click away in the account and the email. The brands that bury cancellation see it come back as a chargeback. The ones that make it obvious lose a few cancels and keep their dispute ratio clean. More on the handling in ecommerce subscription cancellation management.

6. Turn on the basic fraud controls

Now the actual fraud layer. About 77% of merchants increased their use of authentication tools like 3D Secure heading into 2026, and for good reason: AVS, CVV checks, and 3DS catch a meaningful slice of criminal fraud and shift liability on a lot of it.

Require CVV on one-time card payments, reject hard on AVS and CVV mismatch, and enable 3DS where it won't kill conversion. Just be clear about what this layer does and doesn't do. It stops stolen-card fraud. It does not stop the friendly-fraud and service-failure disputes that make up the majority of your volume. Don't let a fraud tool convince you the problem is solved. For help-desk-side coverage, our refund fraud prevention on Shopify guide is the companion piece.

7. Wire up chargeback alerts

Alert networks like Verifi (RDR and CDRN) and Ethoca let an issuer flag an incoming dispute before it becomes a formal chargeback, so you can refund the customer and stop the dispute from ever hitting your ratio.

For a brand near a monitoring threshold, this is the emergency brake. You eat the refund, but you avoid the fee, the representment cost, and the dispute-ratio damage. Treat alerts as triage, not strategy: they buy you time while you fix the triggers upstream. The landscape of options is in our roundup of chargeback management tools.

8. Watch your dispute ratio against VAMP before April 2026

This is the move with a deadline. Visa's Acquirer Monitoring Program tightens its enforcement on April 1, 2026, with a merchant VAMP ratio threshold of 1.5% (150 basis points), and acquirer-level thresholds that start flagging trouble far lower (Forter, Sift).

Cross the line and you're not just paying fees. You risk your acquirer putting you in a monitoring program or, worst case, losing the merchant account that runs your whole business. Know your current dispute ratio. If it's drifting toward the threshold, every move above moves from "good practice" to "do it this quarter." Our breakdown of the acceptable Shopify chargeback percentage covers where the lines sit, and ecommerce chargeback prevention gives the broader playbook.

Want a read on which of these is leaking the most disputes for your store? Book a 30-min call and we'll map your after-hours call volume against your dispute window, live.

What this costs you vs what reachability costs

The after-hours coverage that prevents service-failure disputes is the same coverage that takes work off your CS payroll, so it pays for itself twice. Here's the shape of it for a typical $50M Shopify brand running a 6-rep CS team.

| Line item | Today | With Ringly |

|---|---|---|

| 6 reps × $4K loaded per rep | $24,000/mo | n/a |

| Ringly Enterprise (~$5K/mo) | n/a | $5,000/mo |

| Net monthly CS spend | $24,000/mo | $5,000/mo |

| Monthly savings | n/a | $19,000/mo |

| Annual savings | n/a | $228,000/yr |

That's roughly 70% of repeatable calls (order status, returns, the same questions over and over) routed to the AI, resolved at about $0.42 per call against the $7-$16 a human-handled call runs at the industry BPO average. The other 30%, the genuinely complex calls, still go to your team.

Now stack the dispute side on top. Every one of those answered calls is a call that didn't roll to voicemail and didn't become a chargeback. You're not choosing between "cut support cost" and "reduce chargebacks." Reachability does both. If you want to see your own numbers, book a 30-min call and we'll do the math against your call volume.

Frequently asked questions

What's an acceptable chargeback rate before I get penalized? Visa's VAMP merchant threshold sits at 1.5% (150 basis points) under the stricter enforcement starting April 2026, and acquirers start raising flags well below that. Practically, you want to keep your dispute ratio comfortably under 1%. Cross the line repeatedly and you risk fees or losing your merchant account.

Is it better to fight chargebacks or prevent them? Prevent them. The average merchant nets back only about 1 in 8 of the disputes they fight once you count second chargebacks and the cost of representment. Every dispute you prevent is worth roughly eight times one you contest after the fact.

Can customer service actually reduce chargebacks? Yes, and it's one of the most underused levers. Card networks require the customer to try the merchant before disputing, so being reachable directly heads off disputes. 85% of consumers who feel ignored by support say they're more likely to file a chargeback.

What's the difference between a dispute and a chargeback? A dispute is the customer questioning a charge with their bank. A chargeback is the formal reversal that follows if the dispute isn't resolved in the merchant's favor. The window between the two is where prevention and alerts can still save you.

How does answering the phone reduce chargebacks specifically? Most service-failure disputes start with a customer who couldn't reach you and went to the bank instead. Answering the call, day or night, lets you resolve the issue (give tracking, process a return) before it ever becomes a dispute. That's why after-hours coverage moves the number.

Does 3D Secure stop friendly fraud? No. 3DS and AVS/CVV checks stop criminal, stolen-card fraud and shift some liability, but they do nothing about friendly fraud or service failures, which are the majority of disputes. You need clarity and reachability for those, not authentication.

How fast do I need to respond to prevent a dispute? Fast enough that the customer reaches you before they reach their bank, which often means the same evening or weekend the problem appears. The delay between "I can't reach them" and "I'll just dispute it" is short, so coverage during off-hours matters more than a faster daytime reply.

Talk to us

If you run a $10M-$100M Shopify brand and your dispute ratio is creeping up, the fastest fix isn't another fraud tool. It's making sure the customer can reach you in the moment they'd otherwise call their bank. A 30-min call is the quickest way to see how many of your after-hours calls are turning into disputes.

The 3-layer guarantee.

- Live in 14 days or it's free until launched.

- 65% resolution in 90 days or we refund the last 3 months of subscription fees.

- We keep working free until we hit 65%.

Ruben (Ringly co-founder) takes these calls personally.