This post in 30 seconds.

- Gorgias has raised about $104 million from 23 investors, including Alven, Sapphire Ventures, SaaStr, CRV, Transpose Platform, and Shopify, across rounds from 2019 to 2024.

- Its valuation actually fell from $710M in 2022 to roughly $530M in 2024, even as revenue grew, which tells you something about the pressure it's under to monetize.

- If you run a $10M to $100M Shopify brand and you're already paying Gorgias (or weighing it), the cap table matters because it predicts where your bill is headed: per-resolution AI billing.

You probably didn't go looking for your helpdesk vendor's funding history for fun. You're doing the thing every operator does before they re-sign a contract or add a new tool: checking whether the company behind it is stable, who controls it, and whether the price you pay this year is the price you'll pay next year.

That's the right instinct. For a Shopify brand doing $10M to $100M with a 3 to 12 person support team, your helpdesk isn't a side tool. It's where your CS payroll, your WISMO load, and your customer relationships all live. So who funds Gorgias, and what does their money want? Below is the full sourced picture, plus the angle the database profiles skip: what venture funding actually does to the invoice you pay.

I'm Ruben, co-founder of Ringly.io. We run AI phone support for more than 50 Shopify brands, which means I read vendor cap tables for a living during procurement conversations. If you want to skip the reading and have me walk through your own support numbers, book a 30-min call and we'll do the math on your current setup live.

Gorgias funding at a glance

Gorgias was founded in 2015 in San Francisco by Romain Lapeyre (CEO) and Alex Plugaru (CTO). It's a Shopify-native helpdesk, and over six rounds it has raised about $104 million from 23 investors, according to Crunchbase.

Here's the round-by-round history, with the figures and lead investors each press release and tracker actually reports.

| Round | Date | Amount | Valuation | Lead / notable investors |

|---|---|---|---|---|

| Seed | 2017-2018 | ~$1.5M | n/a | Alven (early backer) |

| Series A | Nov 2019 | $14M | n/a | Alven |

| Series B | Dec 2020 | $25M | n/a | Sapphire Ventures (Rajeev Dham); SaaStr, Alven |

| Series C | Aug 2022 | $30M | $710M | Transpose Platform + Shopify; SaaStr, Sapphire, CRV, Alven |

| Series C-2 | May 2024 | $29M | ~$530M | SaaStr + Alven; Horsley Bridge, Amplify, Shopify, Sapphire, CRV |

The headline number to remember is the valuation line, not the total raised: $710 million in 2022, down to roughly $530 million in 2024. That direction is the whole story, and we'll get to why it matters for you.

At the 2022 Series C, Gorgias was serving around 10,000 stores with 245 employees across seven offices, TechCrunch reported. Today the company says it's past 15,000 merchants, with 40% of Shopify's top 1,500 brands on the platform. If you want the current customer math in detail, we keep a running count in our breakdown of how many merchants Gorgias has, and the revenue picture in our note on Gorgias ARR in 2025.

Who actually invests in Gorgias

The investor list reads like a who's who of B2B SaaS money, which is worth knowing because each type of backer wants something different from the company, and those wants eventually shape the product and the price.

- Alven led the Series A and has been in since the early days. A European venture firm with a patient, repeat-backer profile, the kind of investor that signals continuity rather than a quick flip.

- Sapphire Ventures (Rajeev Dham) led the $25M Series B in December 2020, per Gorgias's own announcement. Sapphire is a growth-stage firm that expects a clear path to scale and, eventually, an exit.

- SaaStr (Jason Lemkin) and CRV are recurring names, in since the B and C rounds. SaaStr in particular is a signal that the company is being coached on the classic SaaS playbook: expand revenue per account, push net revenue retention above 100%.

- Transpose Platform co-led the 2022 Series C.

- Amplify joined at the Series C-2, with partner Sunil Dhaliwal taking a board observer seat. Board observers watch the numbers; they don't join for fun.

- Shopify is the one to pay attention to. Shopify is both a Gorgias integration partner and an investor, in since the Series C.

That last one is the interesting signal. When your platform owner also owns a slice of your helpdesk vendor, you've got a strategic relationship that can cut two ways: tighter integration on one hand, or a future where the partner becomes an acquirer on the other. I'm not predicting an acquisition. I'm saying that if you're signing a multi-year contract, a strategic investor on the cap table is a variable worth noting, not ignoring.

It's also worth separating the two groups Crunchbase counts. Of the 23 investors, most are institutional funds (Alven, Sapphire, SaaStr, CRV, Transpose, Horsley Bridge, Amplify, Shopify) and a handful are angels who came in early. Institutional money at this stage wants growth and margin, not a lifestyle business. That's not a criticism. It's just the math of who's at the table.

Venture-backed vendors don't raise money to keep prices flat. They raise it to grow revenue per customer, and that pressure eventually reaches your account. Hold that thought.

The valuation reset nobody mentions

Here's the number the database profiles list but never explain. Gorgias was valued at $710 million in August 2022. By its May 2024 round, the reported valuation was roughly $530 million, according to equity research firm Sacra.

The company grew revenue the whole time. Sacra puts annual recurring revenue at about $25M in 2022, $51M in 2023, and $69M in 2024, up 34% year over year. So revenue nearly tripled while the valuation dropped by about a quarter.

That's not a Gorgias-specific problem. It's the 2022-to-2024 software multiple reset that hit the whole vertical SaaS category, when interest rates rose and investors stopped paying 30x revenue for growth. But it has a real consequence for the company's behavior. Sacra pegs the May 2024 round at roughly an 8.8x forward revenue multiple, and a growth rate that's slowed from "more than doubling" to 34%.

Think about what that combination does to a board. You raised your last round below your prior valuation. Your growth rate is half what it was. You're sitting on fresh cash and a base of 15,000 paying merchants. The path back to a higher valuation isn't a new logo land grab, it's getting more revenue out of the customers you already have.

A vendor whose growth is decelerating and whose valuation got reset has exactly one lever left that's fully in its control: monetize the existing customer base harder. For a helpdesk, that means raising the average revenue per merchant. And the cleanest way to do that in 2026 is to bill for AI.

What venture funding means for the bill you pay

This is the part the cap-table databases skip, and it's the part that actually touches your P&L.

Look at what the last round was for. The $29 million Series C-2 in May 2024 was raised explicitly to expand Gorgias's AI product, Automate, with the stated goal of deflecting at least 60% of support, as Gorgias announced. Investors funded an AI thesis. Companies monetize the theses they raise on. So the question for you is simple: how does Gorgias charge for that AI?

Per resolution. New Gorgias accounts pay roughly $0.90 for every conversation the AI Agent fully resolves, and overage runs about $1.50 per interaction once you pass your plan's allotment. There's also a double-billing mechanic that catches people off guard: an AI resolution can also consume a billable helpdesk ticket, so the same conversation can be charged twice. We broke the whole model down in our guide to Gorgias AI Agent pricing per resolution, and the full Gorgias pricing breakdown covers the plan tiers.

The complaints write themselves once the volume scales. One Shopify App Store reviewer reported about $14,000 in unexpected AI Agent charges on top of a $13,500 annual Advanced plan. That's the per-resolution model doing exactly what it was designed to do, which is convert your support volume into the vendor's revenue.

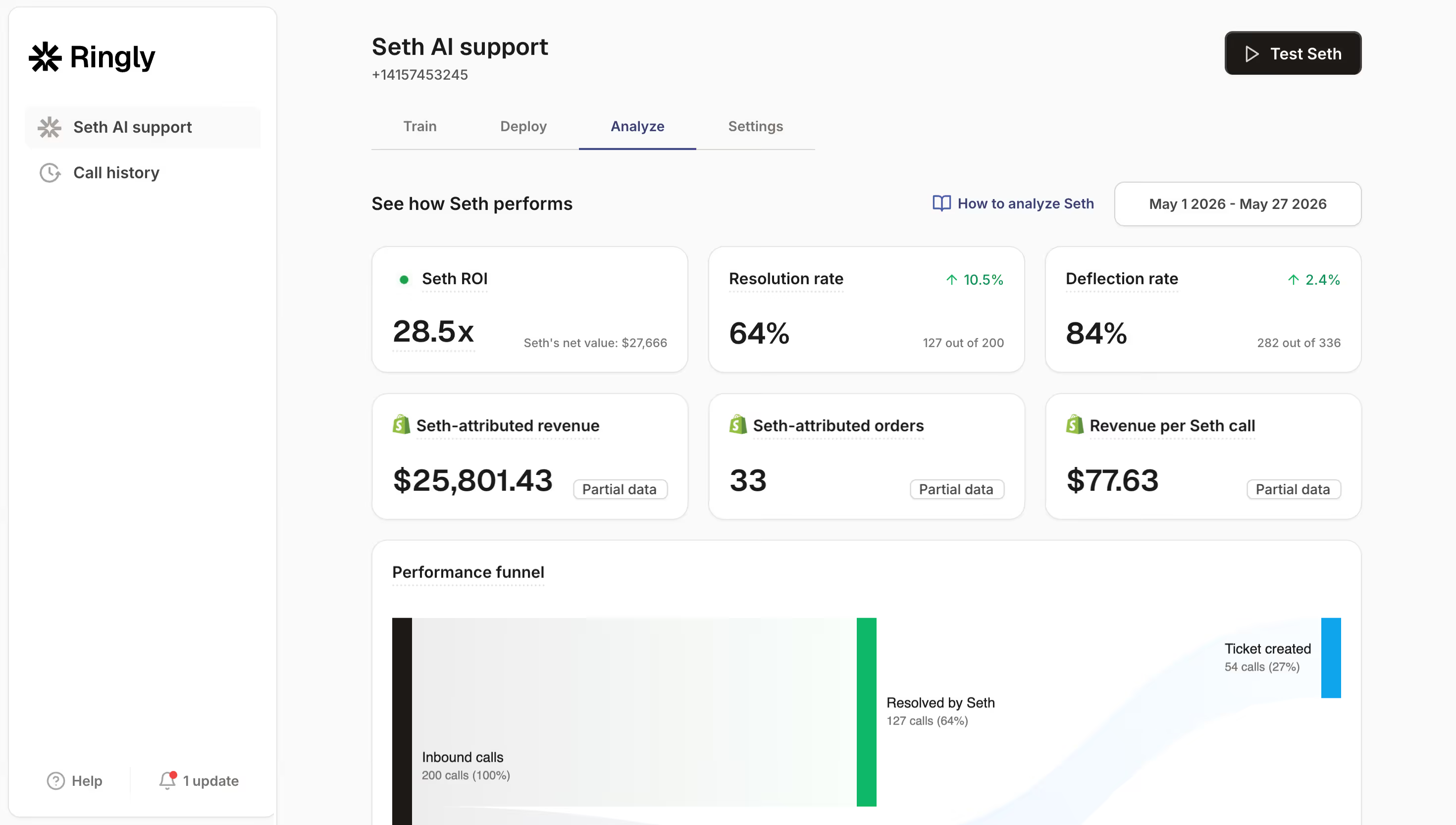

Here's how I read it, having watched this pattern across 50+ brands. A usage-priced vendor's incentive is for your volume to go up, because your volume is their revenue. A flat-priced vendor's incentive is the opposite. When we run AI phone support for a brand, a resolved call costs about $0.42 on a flat plan, no matter how busy the phone gets. WashCo, a Shopify brand we launched, ran its calls at $0.91 each in the first week, versus the $2.70 a human-handled call was costing them. The number doesn't climb with the seasonal spike. That's a different cost shape than per-resolution, and it's the shape I'd want when call volume is unpredictable.

None of this means Gorgias is a bad helpdesk. It's a strong one for ticketing and chat. It means the funding history and the pricing model are connected, and you should price the next year of your contract with that connection in mind. If you want to compare the two cost shapes against your real numbers, book a 30-min call and we'll run it side by side.

How to read a vendor's funding before you sign

You don't need to be a venture analyst to do this. When I'm helping an operator think through a support stack, here's the short checklist I actually use.

- Funding stage and valuation direction. A flat or rising valuation signals a company growing into its price. A reset valuation (like Gorgias going from $710M to $530M) signals monetization pressure. Neither is disqualifying. It just tells you to read the pricing terms harder.

- Pricing model. Flat or usage-based? Usage and per-resolution billing means your costs scale with your busiest months, which are exactly when you can least afford a surprise. Ask for a worked example at your real ticket volume, not the demo volume.

- Strategic investors on the cap table. A platform owner like Shopify holding equity is a partnership signal and an acquisition-risk signal at the same time. Worth a question, not a panic.

- Growth rate. Decelerating growth plus a big cash raise usually means the vendor will work harder to expand revenue per account. That account is you.

- Lock-in and guarantee terms. Annual prepay, overage rates, and whether there's any resolution guarantee. If a vendor charges per outcome, ask what happens when the outcome is wrong and who eats the cost.

"My customers also feel like it's a normal person. They feel like they can communicate if they have questions."

Claudia Droge, TechCraft Studio

That checklist is vendor-agnostic. Run it on Gorgias, run it on us, run it on anyone. The point is that the cap table isn't trivia. It's a leading indicator of your future invoice. For the operator's view of the same tension from the finance seat, our piece on what a CFO should know about Gorgias is worth a read, and if you're weighing whether to keep building the team at all, scaling customer service without hiring covers the operator math.

Where Ringly fits if you're rethinking the stack

To be straight with you: Ringly isn't a Gorgias replacement, and I'd be suspicious of anyone who told you it was. Ringly.io is AI phone support for Shopify brands. It sits in front of your helpdesk and handles the inbound calls, the order-status questions, the returns, the same questions over and over, then escalates cleanly to Gorgias or whatever helpdesk you already run.

The difference operators notice is the cost shape. Across 50+ brands the AI resolves about 73% of calls autonomously at roughly $0.42 per resolved call, on a flat monthly plan, not a per-resolution meter. And it's backed by a 65% resolution guarantee: if the AI resolves under 65% of your calls in 90 days, we refund the last three months. If you've ever watched a support bill climb with your volume during a launch or the holiday spike, that's the structural fix.

If you're weighing the broader market, our roundup of Gorgias alternatives covers the field honestly. For the phone-specific case, see AI phone support for $10M+ Shopify brands, our overview of ecommerce phone support, and the broader picture in ecommerce customer service.

Frequently asked questions

Who are Gorgias's investors? Gorgias's backers include Alven, Sapphire Ventures, SaaStr, CRV, Transpose Platform, Horsley Bridge, Amplify, and Shopify. Alven led the Series A, Sapphire led the Series B, and Transpose and Shopify co-led the 2022 Series C.

How much has Gorgias raised in total? About $104 million across six rounds from 23 investors, per Crunchbase, from a 2019 Series A through a $29 million Series C-2 in May 2024. Some trackers cite a slightly higher figure, but $104M is the most widely reported total.

What is Gorgias's valuation? Gorgias was valued at $710 million at its 2022 Series C and at roughly $530 million at its May 2024 round, according to Sacra. The valuation fell even as revenue grew, reflecting the broader 2022-to-2024 software multiple reset.

How big is Gorgias's revenue? Sacra estimates annual recurring revenue of about $69 million in 2024, up 34% year over year from roughly $51 million in 2023. Growth has slowed from the doubling it posted in earlier years.

Is Gorgias owned by Shopify? No. Shopify is a minority investor and integration partner, not the owner. That said, a platform owner holding equity in a helpdesk vendor is a strategic relationship worth noting if you're signing a long contract.

Does Gorgias being venture-funded make it more expensive? Not automatically, but venture-funded vendors are under pressure to grow revenue per customer, and Gorgias monetizes its AI on a per-resolution basis (roughly $0.90 per resolved conversation, with overage around $1.50). Price your contract knowing that incentive exists.

Talk to us

If you run a $10M to $100M Shopify brand and you're rethinking what you pay for support, a 30-min call is the fastest way to see the two cost shapes side by side: per-resolution billing versus a flat plan, against your real call volume.

The 3-layer guarantee.

- Live in 14 days or it's free until launched.

- 65% resolution in 90 days or we refund the last 3 months of subscription fees.

- We keep working free until we hit 65%.

Ruben (Ringly co-founder) takes these calls personally.